Stationary stochastic process

stochastic process, homogeneous in time

2020 Mathematics Subject Classification: Primary: 60G10 [MSN][ZBL]

A stochastic process  whose statistical characteristics do not change in the course of time

whose statistical characteristics do not change in the course of time  , i.e. are invariant relative to translations in time:

, i.e. are invariant relative to translations in time:  ,

,  , for any fixed value of

, for any fixed value of  (either a real number or an integer, depending on whether one is dealing with a stochastic process in continuous or in discrete time). The concept of a stationary stochastic process is widely used in applications of probability theory in various areas of natural science and technology, since these processes accurately describe many real phenomena accompanied by unordered fluctuations. For example, the pulsations of the force of a current or the voltage in an electrical chain (electrical "noise" ) can be considered as stationary stochastic processes if the chain is in a stationary system; the pulsations of velocity or pressure at a point of a turbulent flow are stationary stochastic processes if the flow is stationary, etc.

(either a real number or an integer, depending on whether one is dealing with a stochastic process in continuous or in discrete time). The concept of a stationary stochastic process is widely used in applications of probability theory in various areas of natural science and technology, since these processes accurately describe many real phenomena accompanied by unordered fluctuations. For example, the pulsations of the force of a current or the voltage in an electrical chain (electrical "noise" ) can be considered as stationary stochastic processes if the chain is in a stationary system; the pulsations of velocity or pressure at a point of a turbulent flow are stationary stochastic processes if the flow is stationary, etc.

In the mathematical theory of stationary stochastic processes, an important role is played by the moments of the probability distribution of the process  , and especially by the moments of the first two orders — the mean value

, and especially by the moments of the first two orders — the mean value  , and its covariance function

, and its covariance function  , or, equivalently, the correlation function

, or, equivalently, the correlation function  . In much of the research into the theory of stationary stochastic processes, the properties that are completely defined by the characteristics

. In much of the research into the theory of stationary stochastic processes, the properties that are completely defined by the characteristics  and

and  alone are studied (the so-called correlation theory or theory of second-order stationary stochastic processes). Accordingly, the stochastic processes

alone are studied (the so-called correlation theory or theory of second-order stationary stochastic processes). Accordingly, the stochastic processes  for which

for which  and

and  do not depend on

do not depend on  are often separated into a special class and are called stationary stochastic processes in the wide sense. The more special stochastic processes, none of whose characteristics change with time (so that the distribution function

are often separated into a special class and are called stationary stochastic processes in the wide sense. The more special stochastic processes, none of whose characteristics change with time (so that the distribution function  of an

of an  -dimensional random variable

-dimensional random variable  depends here, for any

depends here, for any  , only on the

, only on the  differences

differences  ) are called stationary stochastic processes in the strict sense. Accordingly, the theory of stationary stochastic processes is divided into the theory of stationary stochastic processes in the strict sense and in the wide sense, with a different mathematical apparatus used in each.

) are called stationary stochastic processes in the strict sense. Accordingly, the theory of stationary stochastic processes is divided into the theory of stationary stochastic processes in the strict sense and in the wide sense, with a different mathematical apparatus used in each.

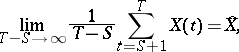

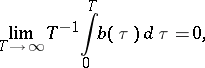

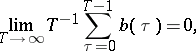

In the strict sense, the theory can be stated outside the framework of probability theory as the theory of one-parameter groups of transformations of a measure space that preserve the measure; this theory is very close to the general theory of dynamical systems (cf. Dynamical system) and to ergodic theory. The most important general theorem of the theory of stationary stochastic processes in the strict sense is the Birkhoff–Khinchin ergodic theorem, according to which for any stationary stochastic process  in the strict sense having a mathematical expectation (i.e.

in the strict sense having a mathematical expectation (i.e.  ), the limit

), the limit

| (1) |

or

| (1a) |

exists with probability 1 (formula (1) relates to processes in continuous time, while (1a) relates to processes in discrete time). There is a result of E.E. Slutskii [Sl], related to stationary stochastic processes in the wide sense, which states that the limit (1) or (1a) exists in mean square. This limit coincides with  if and only if

if and only if

| (2) |

or

| (2a) |

where

|

(the von Neumann ( -) ergodic theorem). These conditions are satisfied, in particular, when

-) ergodic theorem). These conditions are satisfied, in particular, when  as

as  . The Birkhoff–Khinchin theorem can be applied to various stationary stochastic processes in the strict sense of the form

. The Birkhoff–Khinchin theorem can be applied to various stationary stochastic processes in the strict sense of the form

|

where  is an arbitrary functional of the stationary stochastic process

is an arbitrary functional of the stationary stochastic process  , and is a random variable which has a mathematical expectation; if for all such stationary stochastic processes

, and is a random variable which has a mathematical expectation; if for all such stationary stochastic processes  the corresponding limit

the corresponding limit  coincides with

coincides with  , then

, then  is called a metrically transitive stationary stochastic process. For stationary Gaussian stochastic processes

is called a metrically transitive stationary stochastic process. For stationary Gaussian stochastic processes  , the condition of being stationary in the strict sense coincides with the condition of being stationary in the wide sense; metric transitivity will occur if and only if the spectral function

, the condition of being stationary in the strict sense coincides with the condition of being stationary in the wide sense; metric transitivity will occur if and only if the spectral function  of

of  is a continuous function of

is a continuous function of  (see, for example, [R], [CL]). There are, in general, no simple necessary and sufficient conditions for the metric transitivity of a stationary stochastic process

(see, for example, [R], [CL]). There are, in general, no simple necessary and sufficient conditions for the metric transitivity of a stationary stochastic process  .

.

Apart from the above result relating to metric transitivity, there are also other results specifically for stationary Gaussian stochastic processes. For these processes, detailed studies have been made of the question of the local properties of the realizations of  (i.e. of individual observed values), and of the statistical properties of the sequence of zeros or maxima of the realizations of

(i.e. of individual observed values), and of the statistical properties of the sequence of zeros or maxima of the realizations of  , and the points of intersection of it with a given level (see, for example, [CL]). A typical example of the results related to intersections with a level is the statement that, given broad regularity conditions, the set of points of intersection of a high level

, and the points of intersection of it with a given level (see, for example, [CL]). A typical example of the results related to intersections with a level is the statement that, given broad regularity conditions, the set of points of intersection of a high level  with the stationary Gaussian stochastic process

with the stationary Gaussian stochastic process  in a certain special time scale (dependent on

in a certain special time scale (dependent on  and tending rapidly to infinity when

and tending rapidly to infinity when  ) converges to a Poisson flow of events of unit intensity when

) converges to a Poisson flow of events of unit intensity when  (see [CL]).

(see [CL]).

When studying stationary stochastic processes in the wide sense, the Hilbert space  of linear combinations of values of the process

of linear combinations of values of the process  and the mean-square limits of sequences of such linear combinations are examined, and a scalar product is defined in it by the formula

and the mean-square limits of sequences of such linear combinations are examined, and a scalar product is defined in it by the formula  . In this case, the transformation

. In this case, the transformation  , where

, where  is a fixed number, will generate a linear unitary operator

is a fixed number, will generate a linear unitary operator  mapping the space

mapping the space  onto itself; the family of operators

onto itself; the family of operators  clearly satisfies the condition

clearly satisfies the condition  , while the values

, while the values  form a set of points (a curve if the time

form a set of points (a curve if the time  is continuous, and a countable sequence of points if the time is discrete), mapped onto itself by all operators

is continuous, and a countable sequence of points if the time is discrete), mapped onto itself by all operators  . Accordingly, the theory of stationary stochastic processes in the wide sense can be reformulated in terms of functional analysis as the study of the sets of points

. Accordingly, the theory of stationary stochastic processes in the wide sense can be reformulated in terms of functional analysis as the study of the sets of points  of the Hilbert space

of the Hilbert space  , where

, where  is a family of linear unitary operators such that

is a family of linear unitary operators such that  (cf. also Semi-group of operators).

(cf. also Semi-group of operators).

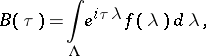

Spectral considerations, based on the expansion of the stochastic process  and its correlation function

and its correlation function  into a Fourier–Stieltjes integral, are central to the theory of stationary stochastic processes in the wide sense. By Khinchin's theorem [Kh] (which is a simple consequence of Bochner's analytic theorem on the general form of a positive-definite function), the correlation function

into a Fourier–Stieltjes integral, are central to the theory of stationary stochastic processes in the wide sense. By Khinchin's theorem [Kh] (which is a simple consequence of Bochner's analytic theorem on the general form of a positive-definite function), the correlation function  of a stationary stochastic process in continuous time can always be represented in the form

of a stationary stochastic process in continuous time can always be represented in the form

| (3) |

where  is a bounded monotone non-decreasing function of

is a bounded monotone non-decreasing function of  , while

, while  ; the Herglotz theorem on the general form of positive-definite sequences similarly shows that the same representation, but with

; the Herglotz theorem on the general form of positive-definite sequences similarly shows that the same representation, but with  , also holds for the correlation function of a stationary stochastic process in discrete time. If the correlation function

, also holds for the correlation function of a stationary stochastic process in discrete time. If the correlation function  decreases sufficiently rapidly as

decreases sufficiently rapidly as  (as is most often the case in applications under the condition that by

(as is most often the case in applications under the condition that by  one understands the difference

one understands the difference  , i.e. it is considered that

, i.e. it is considered that  ), then the integral at the right-hand side of (3) becomes an ordinary Fourier integral

), then the integral at the right-hand side of (3) becomes an ordinary Fourier integral

| (4) |

where  is a non-negative function. The function

is a non-negative function. The function  is called the spectral function of

is called the spectral function of  , while the function

, while the function  (in cases where the equality (4) holds) is called its spectral density. Starting from the Khinchin formula (3) (or from the definition of the process

(in cases where the equality (4) holds) is called its spectral density. Starting from the Khinchin formula (3) (or from the definition of the process  in the form of the set of points

in the form of the set of points  in the Hilbert space

in the Hilbert space  , and Stone's theorem on the spectral representation of one-parameter groups of unitary operators in a Hilbert space), it can also be demonstrated that the process

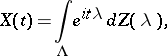

, and Stone's theorem on the spectral representation of one-parameter groups of unitary operators in a Hilbert space), it can also be demonstrated that the process  itself permits a spectral decomposition in the form

itself permits a spectral decomposition in the form

| (5) |

where  is a random function with uncorrelated increments (i.e.

is a random function with uncorrelated increments (i.e.  when

when  ) which satisfies the condition

) which satisfies the condition  , while the integral at the right-hand side is understood to be the mean-square limit of the corresponding sequence of integral sums. The decomposition (5) provides grounds for considering any stationary stochastic process in the wide sense as a superposition of a set of non-correlated harmonic oscillations of different frequencies with random amplitudes and phases; the spectral function

, while the integral at the right-hand side is understood to be the mean-square limit of the corresponding sequence of integral sums. The decomposition (5) provides grounds for considering any stationary stochastic process in the wide sense as a superposition of a set of non-correlated harmonic oscillations of different frequencies with random amplitudes and phases; the spectral function  and the spectral density

and the spectral density  define the distribution of the average energy (or, more accurately, of the power) of the harmonic oscillations with frequency spectrum

define the distribution of the average energy (or, more accurately, of the power) of the harmonic oscillations with frequency spectrum  that constitute

that constitute  (as a result of which the function

(as a result of which the function  in applied research is often called the energy spectrum, or power spectrum, of

in applied research is often called the energy spectrum, or power spectrum, of  ).

).

The spectral decomposition of the correlation function  , defined by formula (3), demonstrates that the mapping

, defined by formula (3), demonstrates that the mapping  , which maps elements

, which maps elements  of the Hilbert space

of the Hilbert space  to elements

to elements  of the Hilbert space

of the Hilbert space  of complex-valued functions on the set

of complex-valued functions on the set  with a modulus, square-integrable with respect to

with a modulus, square-integrable with respect to  , is an isometric mapping of

, is an isometric mapping of  into

into  . This mapping can be extended to an isometric linear mapping

. This mapping can be extended to an isometric linear mapping  of the whole space

of the whole space  onto the space

onto the space  , a fact that allows one to reformulate many problems in the theory of stationary stochastic processes in the wide sense as problems in function theory.

, a fact that allows one to reformulate many problems in the theory of stationary stochastic processes in the wide sense as problems in function theory.

A significant part of the theory of stationary stochastic processes in the wide sense is devoted to methods of solving linear approximation problems for such processes, i.e. methods of locating a linear combination of any "known" values of  that best approximates (in the sense of the minimum least-square error) a certain "unknown" value of the same process or any "unknown" random variable

that best approximates (in the sense of the minimum least-square error) a certain "unknown" value of the same process or any "unknown" random variable  . In particular, the problem of optimal linear extrapolation of

. In particular, the problem of optimal linear extrapolation of  consists of finding the best approximation

consists of finding the best approximation  of the value

of the value  ,

,  , that linearly depends on the "past values" of

, that linearly depends on the "past values" of  with

with  ; the problem of optimal linear interpolation consists of finding the best approximation for

; the problem of optimal linear interpolation consists of finding the best approximation for  that linearly depends on the values of

that linearly depends on the values of  , where

, where  runs through all values that do not belong to a specific interval of the time axis (to which

runs through all values that do not belong to a specific interval of the time axis (to which  does belong); the problem of optimal linear filtering can be formulated as the problem of finding the best approximation

does belong); the problem of optimal linear filtering can be formulated as the problem of finding the best approximation  for a certain random variable

for a certain random variable  (which is usually the value for some

(which is usually the value for some  of a stationary stochastic process

of a stationary stochastic process  , correlated with

, correlated with  , whereby

, whereby  most often plays the part of a "signal" , while

most often plays the part of a "signal" , while  is the sum of the "signal" and a "noise"

is the sum of the "signal" and a "noise"  that interferes with it, and the sum is known from the observations) that linearly depends on the values of

that interferes with it, and the sum is known from the observations) that linearly depends on the values of  when

when  (see Stochastic processes, prediction of; Stochastic processes, filtering of; Stochastic processes, interpolation of).

(see Stochastic processes, prediction of; Stochastic processes, filtering of; Stochastic processes, interpolation of).

All these problems reduce geometrically to the problem of projecting a point of the Hilbert space  (or of its extension) orthogonally onto a given subspace of this space. Relying on this geometric interpretation and on the isomorphism of the spaces

(or of its extension) orthogonally onto a given subspace of this space. Relying on this geometric interpretation and on the isomorphism of the spaces  and

and  , A.N. Kolmogorov has deduced general formulas that make it possible to determine the mean-square error of optimal linear extrapolation or interpolation, corresponding to the case where the value of

, A.N. Kolmogorov has deduced general formulas that make it possible to determine the mean-square error of optimal linear extrapolation or interpolation, corresponding to the case where the value of  is unknown only when

is unknown only when  , by means of the spectral function

, by means of the spectral function  of the stationary stochastic process

of the stationary stochastic process  in discrete time

in discrete time  (see [R], [Ko]–[D]). When used for the extrapolation problem, the same results were obtained for processes

(see [R], [Ko]–[D]). When used for the extrapolation problem, the same results were obtained for processes  in continuous time by M.G. Krein and K. Karhunen. N. Wiener [W] demonstrated that the search for the best approximation

in continuous time by M.G. Krein and K. Karhunen. N. Wiener [W] demonstrated that the search for the best approximation  or

or  in the case of problems of optimal linear extrapolation and filtering can be reduced to the solution of a certain integral equation of Wiener–Hopf type, or (when

in the case of problems of optimal linear extrapolation and filtering can be reduced to the solution of a certain integral equation of Wiener–Hopf type, or (when  is discrete) of the discrete analogue of such an equation, which makes it possible to use the factorization method (see Wiener–Hopf equation; Wiener–Hopf method). Problems of optimal linear extrapolation or filtering of a stationary stochastic process

is discrete) of the discrete analogue of such an equation, which makes it possible to use the factorization method (see Wiener–Hopf equation; Wiener–Hopf method). Problems of optimal linear extrapolation or filtering of a stationary stochastic process  in continuous time in the case where not all its past values for

in continuous time in the case where not all its past values for  are known but only its values on a finite interval

are known but only its values on a finite interval  , as well as the problem of optimal linear interpolation of such an

, as well as the problem of optimal linear interpolation of such an  , can be reduced to certain problems of establishing a special form of differential equation (a "generalized string equation" ) by means of its spectrum (see [Kr], [DM]).

, can be reduced to certain problems of establishing a special form of differential equation (a "generalized string equation" ) by means of its spectrum (see [Kr], [DM]).

The above approaches to the solution of problems of optimal linear extrapolation, interpolation and filtering provide sufficiently-simple explicit formulas for the required best approximation  or

or  that can be successfully used in practice only in certain exceptional cases. One important case in which such explicit formulas do exist is the case of a stationary stochastic process

that can be successfully used in practice only in certain exceptional cases. One important case in which such explicit formulas do exist is the case of a stationary stochastic process  with rational spectral density

with rational spectral density  relative to the

relative to the  (if

(if  is discrete) or relative to

is discrete) or relative to  (if

(if  is continuous), which was studied in detail by Wiener [W] (for applications to problems of extrapolation and filtering by values where

is continuous), which was studied in detail by Wiener [W] (for applications to problems of extrapolation and filtering by values where  ). It was subsequently demonstrated that for such stationary stochastic processes with rational spectral density there is also an explicit solution of the problems of linear interpolation, extrapolation and filtering by means of data on a finite interval

). It was subsequently demonstrated that for such stationary stochastic processes with rational spectral density there is also an explicit solution of the problems of linear interpolation, extrapolation and filtering by means of data on a finite interval  (see, for example, [R], [Y]). The simplicity of processes with rational spectral density can be explained by the fact that such stationary stochastic processes (and practically only they) are a one-dimensional component of a multi-dimensional stationary Markov process (see [D2]).

(see, for example, [R], [Y]). The simplicity of processes with rational spectral density can be explained by the fact that such stationary stochastic processes (and practically only they) are a one-dimensional component of a multi-dimensional stationary Markov process (see [D2]).

The concept of a stationary stochastic process permits a whole series of generalizations. One of these is the concept of a generalized stationary stochastic process. This is a generalized stochastic process (cf. Stochastic process, generalized)  (i.e. a random linear functional, defined on the space

(i.e. a random linear functional, defined on the space  of infinitely-differentiable functions

of infinitely-differentiable functions  with compact support), such that either the distribution function of the random vector

with compact support), such that either the distribution function of the random vector  , where

, where  for any positive integer

for any positive integer  , real number

, real number  and

and  , coincides with the probability distribution of the vector

, coincides with the probability distribution of the vector  (a generalized stationary stochastic process in the strict sense), or else

(a generalized stationary stochastic process in the strict sense), or else

|

|

for all  (a generalized stationary stochastic process in the wide sense). A generalized stationary stochastic process in the wide sense

(a generalized stationary stochastic process in the wide sense). A generalized stationary stochastic process in the wide sense  and its correlation functional

and its correlation functional  (or covariance functional

(or covariance functional  ) permit a spectral decomposition related to (2) and (5) (see Spectral decomposition of a random function). Other frequently-used generalizations of the concept of a stationary stochastic process are the concepts of a stochastic process with stationary increments of a certain order and of a homogeneous random field (cf. Random field, homogeneous).

) permit a spectral decomposition related to (2) and (5) (see Spectral decomposition of a random function). Other frequently-used generalizations of the concept of a stationary stochastic process are the concepts of a stochastic process with stationary increments of a certain order and of a homogeneous random field (cf. Random field, homogeneous).

References

| [Sl] | E.E. Slutskii, Selected works , Moscow (1980) pp. 252–268 (In Russian) |

| [R] | Yu.A. Rozanov, "Stationary random processes" , Holden-Day (1967) (Translated from Russian) MR0214134 Zbl 0152.16302 |

| [CL] | H. Cramér, M.R. Leadbetter, "Stationary and related stochastic processes" , Wiley (1967) MR0217860 Zbl 0162.21102 |

| [Kh] | A.Ya. Khinchin, Uspekhi Mat. Nauk : 5 (1938) pp. 42–51 |

| [Ko] | A.N. Kolmogorov, "Interpolation and extrapolation of stationary stochastic series" Izv. Akad. Nauk SSSR Ser. Mat. , 5 : 1 (1941) pp. 3–14 (In Russian) (German abstract) |

| [D] | J.L. Doob, "Stochastic processes" , Wiley (1953) MR1570654 MR0058896 Zbl 0053.26802 |

| [GS] | I.I. Gihman, A.V. Skorohod, "The theory of stochastic processes" , 1 , Springer (1971) (Translated from Russian) MR0636254 MR0651015 MR0375463 MR0346882 Zbl 0531.60002 Zbl 0531.60001 Zbl 0404.60061 Zbl 0305.60027 Zbl 0291.60019 |

| [W] | N. Wiener, "Extrapolation, interpolation and smoothing of stationary time series" , M.I.T. (1949) MR0031213 Zbl 0036.09705 |

| [Kr] | M.G. Krein, "On a basic approximation problem of the theory of extrapolation and filtering of stationary stochastic processes" Dokl. Akad. Nauk SSSR , 94 : 1 (1954) pp. 13–16 (In Russian) |

| [DM] | H. Dym, H.P. McKean, "Gaussian processes, function theory, and the inverse spectral problem" , Acad. Press (1976) MR0448523 Zbl 0327.60029 |

| [Y] | A.M. Yaglom, "Extrapolation, interpolation and filtering of stationary stochastic processes with rational spectral density" Trudy Moskov. Mat. Obshch. , 4 (1955) pp. 333–374 (In Russian) |

| [D2] | J.L. Doob, "The elementary Gaussian processes" Ann. Math. Stat. , 15 (1944) pp. 229–282 MR0010931 Zbl 0060.28907 |

Comments

In the English language literature one says ergodic stationary process rather than metrically-transitive stationary process. See also Gaussian process.

The terminology concerning the phrases "correlation function" and "covariance function" is not yet completely standardized. In probability theory the following terminology seems just about universally adopted. Given two random variables  their covariance is

their covariance is  , their correlation coefficient is

, their correlation coefficient is  , where

, where  is the variance of

is the variance of  ,

,  (cf. Dispersion), and there is no special name for the mixed second-order moment

(cf. Dispersion), and there is no special name for the mixed second-order moment  . Correspondly one has the terms covariance function and correlation function, also termed auto-correlation function and auto-covariance function, for the following quantities associated to a stochastic process:

. Correspondly one has the terms covariance function and correlation function, also termed auto-correlation function and auto-covariance function, for the following quantities associated to a stochastic process:

|

|

and for two stochastic processes  there are correspondingly the cross covariance function and cross correlation function

there are correspondingly the cross covariance function and cross correlation function

|

|

However, in application areas of probability theory a somewhat different terminology is also employed, for instance in oceanology, hydrology and electrical engineering (cf. [J]–[So]). E.g., one also finds the phrase "correlation function" for the quantity  (instead of covariance function). Also, one regularly finds the terminology "correlation function" for the quantity

(instead of covariance function). Also, one regularly finds the terminology "correlation function" for the quantity

|

which is also in agreement with the phrase "correlation function" (pair correlation function) as it is used in statistical mechanics, cf. e.g. [T].

If the process is stationary, the distinctions are minor. Thus, if  ,

,  ,

,  ,

,  .

.

References

| [J] | A.H. Jazwinski, "Stochastic processes and filtering theory" , Acad. Press (1970) pp. 53–54 Zbl 0203.50101 |

| [SSN] | Y. Sawaragi, Y. Sunahara, T. Nakamizo, "Statistical decision theory in adaptive control systems" , Acad. Press (1967) Zbl 0189.47003 |

| [MO] | A.S. Monin, R.V. Ozmidov, "Turbulence in the ocean" , Reidel (1985) (Translated from Russian) |

| [So] | K. Sobczyk, "Stochastic differential equations. With applications to physics and engineering" , Kluwer (1991) pp. 23 MR1135326 Zbl 0762.60050 |

| [T] | C.J. Thompson, "Mathematical statistical mechanics" , Princeton Univ. Press (1972) MR0469020 Zbl 0244.60082 |

Stationary stochastic process. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Stationary_stochastic_process&oldid=26947