Pareto distribution

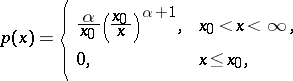

A continuous probability distribution with density

|

depending on two parameters  and

and  . As a "cut-off" version the Pareto distribution can be considered as belonging to the family of beta-distributions (cf. Beta-distribution) of the second kind with the density

. As a "cut-off" version the Pareto distribution can be considered as belonging to the family of beta-distributions (cf. Beta-distribution) of the second kind with the density

|

for  . For any fixed

. For any fixed  , the Pareto distribution reduces by the transformation

, the Pareto distribution reduces by the transformation  to a beta-distribution of the first kind. In the system of Pearson curves the Pareto distribution belongs to those of "type VI" and "type XI" . The mathematical expectation of the Pareto distribution is finite for

to a beta-distribution of the first kind. In the system of Pearson curves the Pareto distribution belongs to those of "type VI" and "type XI" . The mathematical expectation of the Pareto distribution is finite for  and equal to

and equal to  ; the variance is finite for

; the variance is finite for  and equal to

and equal to  ; the median is

; the median is  . The Pareto distribution function is defined by the formula

. The Pareto distribution function is defined by the formula

|

The Pareto distribution has been widely used in various problems of economical statistics, beginning with the work of W. Pareto (1882) on the distribution of profits. It is sometimes accepted that the Pareto distribution describes fairly well the distribution of profits exceeding a certain level in the sense that it must have a tail of order  as

as  .

.

References

| [1] | H. Cramér, "Mathematical methods of statistics" , Princeton Univ. Press (1946) |

Comments

References

| [a1] | N.L. Johnson, S. Kotz, "Distributions in statistics: continuous univariate distributions" , Houghton Mifflin (1970) |

| [a2] | H.T. Davis, "Elements of statistics with application to economic data" , Amer. Math. Soc. (1972) |

Pareto distribution. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Pareto_distribution&oldid=49356