Difference between revisions of "Markov moment"

Ulf Rehmann (talk | contribs) m (MR/ZBL numbers added) |

(refs format) |

||

| Line 39: | Line 39: | ||

====References==== | ====References==== | ||

| − | + | {| | |

| − | + | |valign="top"|{{Ref|GS}}|| I.I. Gihman, A.V. [A.V. Skorokhod] Skorohod, "The theory of stochastic processes" , '''2''' , Springer (1975) (Translated from Russian) {{MR|0375463}} {{ZBL|0305.60027}} | |

| − | + | |} | |

====Comments==== | ====Comments==== | ||

| Line 47: | Line 47: | ||

====References==== | ====References==== | ||

| − | + | {| | |

| + | |valign="top"|{{Ref|BG}}|| R.M. Blumenthal, R.K. Getoor, "Markov processes and potential theory" , Acad. Press (1968) {{MR|0264757}} {{ZBL|0169.49204}} | ||

| + | |- | ||

| + | |valign="top"|{{Ref|Do}}|| J.L. Doob, "Classical potential theory and its probabilistic counterpart" , Springer (1984) pp. 390 {{MR|0731258}} {{ZBL|0549.31001}} | ||

| + | |- | ||

| + | |valign="top"|{{Ref|Dy}}|| E.B. Dynkin, "Markov processes" , '''1''' , Springer (1965) (Translated from Russian) {{MR|0193671}} {{ZBL|0132.37901}} | ||

| + | |- | ||

| + | |valign="top"|{{Ref|W}}|| A.D. Wentzell, "A course in the theory of stochastic processes" , McGraw-Hill (1981) (Translated from Russian) {{MR|0781738}} {{MR|0614594}} {{ZBL|0502.60001}} | ||

| + | |- | ||

| + | |valign="top"|{{Ref|B}}|| L.P. Breiman, "Probability" , Addison-Wesley (1968) {{MR|0229267}} {{ZBL|0174.48801}} | ||

| + | |} | ||

Revision as of 06:28, 14 May 2012

Markov time; stopping time

2020 Mathematics Subject Classification: Primary: 60G40 [MSN][ZBL]

A notion used in probability theory for random variables having the property of independence of the "future" . More precisely, let  be a measurable space with a non-decreasing family

be a measurable space with a non-decreasing family  ,

,  , of

, of  -algebras of

-algebras of  (

( in the case of continuous time and

in the case of continuous time and  in the case of discrete time). A random variable

in the case of discrete time). A random variable  with values in

with values in  is called a Markov moment or Markov time (relative to the family

is called a Markov moment or Markov time (relative to the family  ,

,  ) if for each

) if for each  the event

the event  belongs to

belongs to  . In the case of discrete time this is equivalent to saying that for any

. In the case of discrete time this is equivalent to saying that for any  the event

the event  belongs to

belongs to  .

.

Examples.

1) Let  ,

,  , be a real-valued right-continuous random process given on

, be a real-valued right-continuous random process given on  , and let

, and let  . Then the random variables

. Then the random variables

|

and

|

that is, the (first and first after  ) times of hitting the (Borel) set

) times of hitting the (Borel) set  , form Markov moments (in the case

, form Markov moments (in the case  it is assumed that

it is assumed that  ).

).

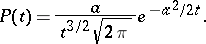

2) If  ,

,  , is a standard Wiener process, then the Markov moment

, is a standard Wiener process, then the Markov moment

|

has probability density

|

Here  , but

, but  .

.

3) The random variable

|

being the first time after which  remains in

remains in  , is an example of a non-Markov moment (a random variable depending on the "future" ).

, is an example of a non-Markov moment (a random variable depending on the "future" ).

Using the idea of a Markov moment one can formulate the strong Markov property of Markov processes (cf. Markov process). Markov moments and stopping times (that is, finite Markov moments) play a major role in the general theory of random processes and statistical sequential analysis.

References

| [GS] | I.I. Gihman, A.V. [A.V. Skorokhod] Skorohod, "The theory of stochastic processes" , 2 , Springer (1975) (Translated from Russian) MR0375463 Zbl 0305.60027 |

Comments

References

| [BG] | R.M. Blumenthal, R.K. Getoor, "Markov processes and potential theory" , Acad. Press (1968) MR0264757 Zbl 0169.49204 |

| [Do] | J.L. Doob, "Classical potential theory and its probabilistic counterpart" , Springer (1984) pp. 390 MR0731258 Zbl 0549.31001 |

| [Dy] | E.B. Dynkin, "Markov processes" , 1 , Springer (1965) (Translated from Russian) MR0193671 Zbl 0132.37901 |

| [W] | A.D. Wentzell, "A course in the theory of stochastic processes" , McGraw-Hill (1981) (Translated from Russian) MR0781738 MR0614594 Zbl 0502.60001 |

| [B] | L.P. Breiman, "Probability" , Addison-Wesley (1968) MR0229267 Zbl 0174.48801 |

Markov moment. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Markov_moment&oldid=23626